How Does the Fed Use Its Monetary Policy Tools to Influence the Economy? (they don't use open market operations to control the federal funds rate)

"The Federal Reserve sets two overnight interest rates: the

interest rate paid on banks' reserve balances and the rate on our

reverse repurchase agreements. We use these two administered rates to

keep a market-

determined rate, the federal funds rate, within a target range set by

the FOMC."

"The Federal Reserve (the Fed)

is the central bank of the United States. As the central bank, it serves

several key functions within the economy. One of the most important

functions of the Fed is to promote economic stability using monetary

policy. The Fed's goals for monetary policy, as defined by Congress, are

to promote maximum employment and price stability.

The Federal Open Market Committee (FOMC) is the monetary

policymaking arm of the Federal Reserve. The FOMC usually meets eight

times per year in Washington, D.C. These two-day meetings include a

review of economic data and financial conditions, briefings by

economists, policy discussions, and a vote on the setting of monetary

policy—including a decision about whether the FOMC will adjust its

target range for the federal funds rate. The federal funds rate is the

interest rate banks charge each other for overnight loans. The Fed sets a

target range for where it wants the interest rates charged to fall

within, and it is the setting of this range that the Fed uses to

communicate its monetary policy position.

Figure 1 The Federal Funds Rate Target Range

SOURCE: Board of Governors of the Federal Reserve System via FRED®, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/graph/?g=COX8, accessed April 4, 2022.

The FOMC conducts monetary policy by

setting the target range for the federal funds rate. This graph shows

the target range, determined by the upper and lower limits, and the

effective federal funds rate within the range.

Over time, as shown in Figure 1,2 the FOMC has moved the

target range up and down as it steers the economy toward maximum

employment and price stability. For example, once the economy recovered

from the global financial crisis, the FOMC moved the target range from

near zero at the end of 2015 up to 2¼ -2½ percent by early 2019. Then

when the COVID-19 pandemic hit, the FOMC quickly moved the target range

back to near zero.

What Is the Federal Funds Rate and Why Is It So Important?

The federal funds rate is a very specific short-term interest rate.

It involves the transfer of funds between banks that maintain accounts

(deposits) with their Federal Reserve Bank; the accounts are called reserve balance

accounts. The federal funds market is where banks that may need money

in their reserve accounts for cashflow reasons go to borrow from banks

that have excess funds in their reserve accounts. Banks who lend funds

act as suppliers of reserves in the federal funds market; banks who

borrow funds act as demanders of reserves in the federal funds market.

The federal funds rate is not "set" by the Fed, but rather determined by

the borrowers and lenders in the federal funds market.

Monetary policy is transmitted through market

interest rates to affect consumers' and producers' spending decisions,

which ultimately moves the economy toward the Fed's objectives—maximum

employment and stable prices. This monetary policy implementation

framework ensures that when the FOMC changes its policy stance (raises

or lowers the target range for the federal funds rate), market interest

rates and financial conditions move in the desired direction.

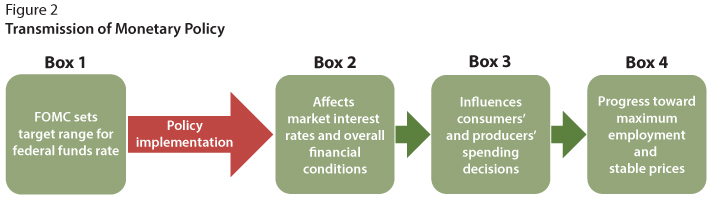

The FOMC conducts monetary policy by setting the target range for the

federal funds rate (Figure 2, Box 1). Then the Fed implements policy by

using its monetary policy tools to ensure the federal funds rate stays

within the target range (red arrow).

The federal funds rate is important because when the FOMC sets its

target range, it influences many other interest rates in the economy

(Figure 2, Box 2). In fact, by adjusting the target for this rate, the

Fed can influence the spending choices of consumers and producers

(Figure 2, Box 3) and ultimately move the economy toward maximum

employment and price stability (Figure 2, Box 4).

The Fed's Monetary Policy Implementation Toolbox

The Fed uses its monetary policy tools in the implementation phase.

In all, the Fed uses four key tools to help ensure the federal funds

rate stays within the target range set by the FOMC.3 We'll

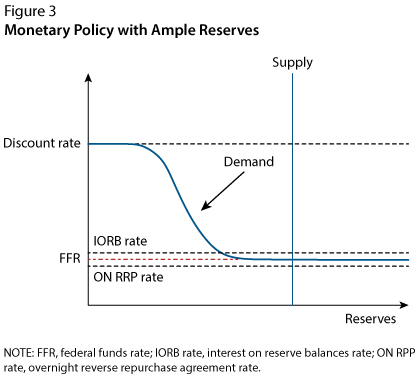

use a simple supply and demand model (Figure 3) to describe how the

tools work together. Overall, these are the critical tools the Fed uses

because reserves in the banking system are ample. That is, the supply of

reserves, set by the Fed, is large enough that it intersects the demand

curve where it is nearly flat (see Figure 3).

In the ample-reserves framework, the Federal Reserve raises (lowers) its administered rates to move the federal funds rate higher (lower). Small shifts of the supply curve have little or no effect on the federal funds rate.

The Fed's Primary Tool: Interest on Reserve Balances

Today, the Fed's primary tool for adjusting the federal funds rate is

interest on reserve balances. The interest on reserve balances rate

(labeled "IORB rate" in Figure 3) is the interest rate paid on funds

that banks hold in their reserve balance account at a Federal Reserve

Bank. For banks, this interest rate represents a risk-free investment

option. Importantly, the interest on reserve balances rate is an

"administered rate," which means it is set by the Fed and not determined

in a market (like the federal funds rate is). In fact, there are two

key concepts that ensure interest on reserves is an effective tool.

The first concept is the reservation rate, which is the lowest

rate that banks are willing to accept for lending out their funds.

Banks can deposit their funds at the Federal Reserve and earn the

interest on reserve balances rate. Because depositing funds at the Fed

is a risk-free option, banks will likely not be willing to lend their

funds in the federal funds market for a lower interest rate than they

can earn from depositing their funds at the Fed. So, the interest on

reserve balances rate serves as a reservation rate for banks.

The second concept is arbitrage, which is the simultaneous

purchase and sale of funds (or goods) in order to profit from a

difference in price. For example, let's assume reserves are trading in

the federal funds market at 2 percent (i.e., the federal funds rate is 2

percent) and that reserves (deposits) at the Fed earn 2.5 percent

(i.e., the interest on reserve balances rate is 2.5 percent). Banks will

quickly see that they can borrow funds in the federal funds market at 2

percent and deposit those funds at the Fed and earn the interest on

reserve balances rate of 2.5 percent, which means that they can earn a

profit of 0.5 percent (the difference between the rates).The increase in

demand for funds in the federal funds market will put upward pressure

on the federal funds rate, and the federal funds rate will rise toward

the interest on reserve balances rate. This upward pressure on the

federal funds rate will continue until the federal funds rate has risen

to the level that banks no longer see the opportunity to profit.

So, arbitrage ensures that the federal funds rate does not fall far below the interest on reserve balances rate.

Arbitrage is the reason why these short-term rates remain closely

linked. In fact, arbitrage is what makes interest on reserve balances an

effective tool for guiding the federal funds rate. Because the Fed sets

the interest on reserve balances rate directly, the Fed can steer the

federal funds rate down or up by lowering or raising the level of the

interest on reserve balances rate. As a result, interest on reserve

balances is the Fed's primary tool for adjusting the federal funds rate,

but the Fed has other tools that play supporting roles.

Setting a Floor for the Federal Funds Rate: The Overnight Reverse Repurchase Agreement Facility

Interest on reserve balances is available only to banks and a few

other institutions. The Fed has an overnight reverse repurchase facility

that is open to a broader set of financial institutions. This facility

allows these financial institutions to deposit their funds at a Federal

Reserve Bank and earn the overnight reverse repurchase agreement rate

offered by the Fed. The overnight reverse repurchase agreement rate

(labeled "ON RRP rate" on Figure 3) works for these institutions similar

to the way the interest on reserve balances rate works for banks. So,

this rate acts like a reservation rate for these financial institutions,

and the overnight reverse repurchase agreement rate interacts with

other short-term market rates through arbitrage. The overnight reverse

repurchase agreement facility is a supplementary tool because the rate

the Fed sets for it helps set a floor for the federal funds rate (Figure

4).

Figure 4 Steering the Federal Funds Rate

SOURCE: Federal Reserve Bank of New York and Board of

Governors of the Federal Reserve System via FRED®, Federal Reserve Bank

of St. Louis;

https://fred.stlouisfed.org/graph/?g=LP47, accessed April 4, 2022.

The Fed implements monetary policy by using

its monetary policy tools, such as the interest of reserve balances

rate (red) and overnight reverse repurchase agreement rate (blue), to

ensure interest rates are consistent with the federal funds rate

target.

Setting a Ceiling for the Federal Funds Rate: The Discount Window

The discount rate is the rate charged by the Fed for loans obtained through the Fed's discount window.

Because banks will not likely borrow at a higher rate than they can

borrow from the Fed, the discount rate acts as a ceiling for the federal

funds rate: It is set higher than the interest on reserve balances rate

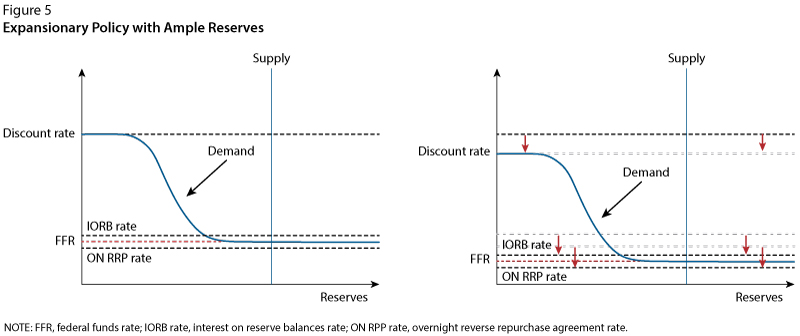

and the overnight reverse repurchase agreement rate (Figure 5).

When the Federal Reserve lowers its administered

rates, the end points of the demand curve shift down. The vertical

supply curve is unchanged. The demand curve intersects the supply curve

at a lower federal funds rate. In general, the Fed tends to lower all

the administered rates by the same amount, keeping the spread between

the rates constant.

The Final Tool: Open Market Operations

As noted above, the Fed's current method for implementing monetary

policy relies on banks' reserves remaining "ample." So, if the Fed needs

to add reserves to ensure they remain ample, it does so by buying U.S.

government securities in the open market. This action is known as open market operations.

When the Fed buys securities, it pays for them by depositing funds into

the appropriate banks' reserve balance accounts, adding to the overall

level of reserves in the banking system. As Figure 3 shows, open market

operations can be used to shift the supply curve left or right. Prior to

2008, open market operations were the Fed's primary monetary policy

tool, which it used daily to make sure the federal funds rate hit the

FOMC's target. Today this tool is mainly used to ensure that reserves

remain ample.

Now that you understand the Fed's implementation tools, let's see how

the Fed uses them to achieve its two goals: maximum employment and

price stability.

Expansionary Monetary Policy Using the Fed's Tools

Suppose the following: The economy weakens, with employment falling

short of maximum employment, and the inflation rate has been steady at

around 2 percent but is showing signs of decreasing. The FOMC might

decide to conduct monetary policy by lowering its target range for the federal funds rate. To implement

that monetary policy, it would decrease its administered rates—the

interest on reserve balances rate, overnight reverse repurchase

agreement rate, and discount rate—to ensure the market-determined

federal funds rate stays within the target range (see Figure 5). These

actions would transmit to other interest rates and broader financial

conditions:

Lower interest rates decrease the cost of borrowing money, which

encourages consumers to increase spending on goods and services and

businesses to invest in new equipment.

The increase in

consumption spending increases the overall demand for goods and services

in the economy, which creates an incentive for businesses to increase

production, hire more workers, and spend more on other resources.

As

these increases in spending ripple through the economy, likely moving

the unemployment rate down toward its full employment level, inflation

could possibly move up.

So, the Fed's monetary policy implementation tools can be effective

for moving the economy back toward maximum employment and price

stability when the economy is stalling.

Contractionary Monetary Policy Using the Fed's Tools

Suppose the following: The economy is showing signs of overheating,

with the unemployment rate very low and businesses finding it hard to

fill jobs, and the inflation rate has been above the Fed's 2 percent

target for quite some time and is rising. In this case, the FOMC might

decide to conduct monetary policy by raising its target range for the federal funds rate. To implement

that monetary policy, it would increase its administered rates—the

interest on reserve balances rate, overnight reverse repurchase

agreement rate, and discount rate—to ensure the federal funds rate stays

within the target range. These actions would transmit to other interest

rates and broader financial conditions:

Higher interest rates increase the cost of borrowing money and

raise the incentive to save, which dampens consumer spending on some

goods and services and slows businesses' investment in new equipment.

The

decrease in consumption spending decreases the overall demand for goods

and services in the economy, which will likely lead to a decrease in

production levels, fewer employees hired, and less spending on other

resources.

As these decreases in spending ripple through the

economy, demand for workers could lessen, inflationary pressures would

diminish, and the inflation rate would fall back toward 2 percent.

So, higher interest rates can be used to move the economy back to

maximum employment and price stability when the economy is overheating.

Conclusion

The Fed has a congressional mandate of maximum employment and price

stability. The FOMC conducts monetary policy by setting the target range

for the federal funds rate. Then the Fed uses its monetary policy tools

to implement the policy, which guides market interest rates toward the

Fed's desired setting of policy. The Fed ensures there are ample

reserves in the banking system and uses its administered rates to steer

the federal funds rate into the FOMC's target range: Interest on reserve

balances is the Fed's primary tool for adjusting the federal funds

rate; the overnight reverse repurchase agreement facility is a

supplementary tool that sets a floor for the federal funds rate; and the

discount rate serves as a ceiling for the federal funds rate. Changes

in the federal funds rate are transmitted to other interest rates

through arbitrage and affect the decisions of consumers and businesses.

Their decisions ultimately move the economy toward maximum employment

and price stability.

2 The effective federal funds rate is the

rate used in the figures in this article. On any given day, there are

many transactions that settle at slightly different federal funds rates.

The effective federal funds rate is the volume-weighted median rate of

these transactions.

3 The Fed recently introduced two

repurchase agreement (repo) backstop tools, the standing overnight repo

facility and the foreign and international monetary authorities repo

facility. These are used by specific counterparties to help set a

ceiling on repo rates. We do not discuss them here because this article

is targeted toward a principles of economics audience.

Arbitrage: The simultaneous purchase and sale of funds (or goods) in order to profit from a difference in price.

Discount rate: The interest rate charged by the Federal Reserve to banks for loans obtained through the Fed's discount window.

Facility: A standing program targeted at a set of

counterparties for depositing or lending. The Fed has permanent

facilities (like the discount window and the overnight reverse

repurchase agreement facility) as well as temporary facilities (like

those implemented during the Financial Crisis of 2007-09 and the

COVID-19 pandemic).

Federal Open Market Committee (FOMC): A Committee created by

law that consists of the seven members of the Board of Governors; the

president of the Federal Reserve Bank of New York; and, on a rotating

basis, the presidents of four other Reserve Banks. Nonvoting Reserve

Bank presidents also participate in Committee deliberations and

discussion.

Maximum employment: The highest level of employment that an economy can sustain while maintaining a stable inflation rate.

Open market operations: The buying and selling of government

securities through primary dealers by the Federal Reserve. When the

securities are bought or sold, reserves in the banking system are

increased or decreased, respectively.

Price stability: A low and stable rate of inflation maintained over an extended period of time.

Reservation rate: The lowest rate of return that banks are willing to accept for lending out funds.

Reserve balances (reserves): The deposits a bank maintains in its account with a Federal Reserve Bank."

No comments:

Post a Comment