"Americans dined out less as inflation surged this summer, but couldn’t resist shelling out more at coffee and pastry shops.

Total

consumer spending fell 3.1% in June from a year earlier at the

restaurants analyzed in a report by the financial-services provider

Rabobank using data from Earnest Research. But spending at coffee shops

and bakery cafes rose 1.9% during the period, the report said.

Analysts,

economists and coffee drinkers offer varied explanations for the

resilience of caffeine and sugar suppliers, including the pleasure of

relatively small indulgences during a time of belt-tightening."

[One coffee drinker said] "“It’s not really going to eat into my budget if I’m just going every once in a while,”" [when the share of your budget spent on a good is low, its price elasticity of demand will be low so that for any given price change quantity demanded will not change much]

"Many consumers are hooked on their routines as much as the stimulants"

"Some

analysts said the relative health of coffee and pastry purveyors in June

could be a reflection of the return of more workers to offices. “The

basic hypothesis is that when you commute, you will buy more in coffee

shops,” said David Tinsley, senior economist at Bank of America

Institute. “You’re quite likely to buy one going into work. You’re quite

likely to buy your lunch or another cup of coffee in the afternoon.”

The

average price of a cup of a coffee in a quick-service shop was $4.90 in

the first six months of this year, up 7.6% from the same period last

year" [if they are saying that coffee costs 7.6% more than 12 months ago, then that is pretty close to the overall inflation rate so we would not expect sales or quantity demanded to be affected too much]

"Brewing at home was more expensive, too. The price of coffee increased 15.8% in June from a year earlier and rose 20.3% in July, according to the Labor Department." [if coffee you brew at home is a substitute for coffee from a shop then when the price of store bought coffee increases the demand for a substitute will increase. That would help explain why the coffee shops are doing okay]

"Alfredo Romero, economics professor at North Carolina Agricultural and

Technical State University, said, “There are some things that people are

slower to let go of, and one of those things is coffee.”" [that could be consistent with the earlier statement about people being hooked on stimulants which would mean that there are not many good substitutes for coffee and goods with few substitutes have a low price elasticity of demand]

"But one

characteristic of today’s economy is that job cuts at small startups and

large companies have yet to dent the overall labor market. Labor demand

is still historically strong, offering only faint signs of cooling.

There are nearly two job openings for every unemployed person

seeking work. That means many workers who are losing their jobs are

quickly landing jobs. Some are even weighing multiple offers and

accepting positions that pay more and better align with their skills.

“With

unemployment so low, job openings so high and the quits rate so high,

we’re finding that the balance of power is still with the job seeker,”

said Paul McDonald, senior executive director at staffing firm Robert Half.

Initial jobless claims, the number of applications for state unemployment benefits, have risen this summer

after hitting a half-century low in the spring. In the week ended Aug.

13, a seasonally adjusted 250,000 workers filed for benefits, above the

2019 prepandemic average of 218,000 and a sign that layoffs have ticked

up.

Meanwhile, continuing claims, a proxy for the number of people claiming

ongoing jobless benefits, have increased at a much slower rate.

Continuing claims were about 1.4 million in the week ended Aug. 6, below

their 2019 average of 1.7 million. Relatively low and stable continuing

claims could indicate workers are leaving unemployment rolls quickly as

they regain employment, some economists say."

"The typical unemployed worker had been off the job for 8.5 weeks in

July, down from 14.4 weeks a year earlier, according to the Labor

Department. The shorter duration of unemployment suggests many

unemployed Americans are finding jobs fast as fewer leave the labor

force, said Julia Pollak, chief economist at ZipRecruiter.

Shorter episodes of joblessness defy economists’ concerns earlier in the pandemic that workers would suffer from long-term spells of unemployment of 27 weeks or more like they did after the 2007-09 recession.

The share of all jobless Americans unemployed for less than five weeks

surpassed the share of those out of work for at least 27 weeks in

January, according to the Labor Department. The gap has since widened.

By July, nearly 37% of unemployed workers had been out of work less than

five weeks, roughly double the percentage experiencing long-term

joblessness."

"Employers

had 10.7 million unfilled jobs in June, down from a record of 11.9

million in March, but still well above the 7 million job openings in

February 2020 ahead of the pandemic, when the labor market was also

booming.

Job-openings

rates across industries are much higher than before the pandemic hit,

suggesting companies still need workers even in sectors where company

layoffs have been pronounced, such as technology, real estate, finance

and insurance.

Longer periods of unemployment can allow job seekers more time to search for roles that match their skill sets,

some economists say. But with job opportunities so abundant, many

unemployed workers are finding jobs that suit them within a matter of

weeks or even days."

Attendance remains below prepandemic levels, but Disneyland and Disney World are making more money than ever. The company has raised some prices and eliminated or started charging for other services and features that used to be free.

"These days, Walt Disney Co. DIS -2.89%▼ has a new magic trick: wringing every last dollar out of each visitor to its profitable theme parks."

"The results reflect a major strategic shift on Disney’s part, where the

company is focused less on maximizing the quantity of visitors and more

on increasing how much money each visitor spends, an approach the

company refers to as yield management. Improving the visitor experience,

the thinking goes, will prompt guests to spend more hours—and therefore

more money—at the parks because they are having such a good time."

"The

biggest change in the past two years—and the most lucrative for

Disney—is the introduction of a smartphone-app feature called Genie+

that costs $15 per person a day, on top of the price of admission, and

allows parkgoers to skip the unreserved lines for some attractions,

which the company refers to as “standby.” But Genie+ doesn’t cover

everything. To skip the standby lines at the most sought-after

attractions, including some Star Wars and Guardians of the Galaxy-themed

rides, reservations now cost an additional $10 to $17. Standby waits

for popular attractions can last hours.

At the same time, many benefits that used to be free—from

parking for certain annual passholders to airport shuttles to MagicBand

wristbands that serve as combination hotel-room keys and park

passes—have been eliminated or now come with a price."

"Disney’s theme-park pricing is determined by “pure supply and demand,”

said a company spokeswoman. “No different than airplanes, hotels or

cruise ships.”"

"annual passholders at Disneyland account for about one half of annual

visits—but . . . annual passholders tend to spend less than

other visitors per visit"

"A typical annual pass holder might ride only one ride during a visit,

eat an ice cream cone and walk around for a few hours, taking up

capacity that might otherwise be used by out-of-state visitors"

"About half of visitors to the parks pay for and use Genie+"

"of those who pay for Genie+, 70% say in post-visit surveys that they plan to do so again"

"Disney has stopped selling nearly all new annual passes to Disneyland

and Walt Disney World and has done away with a host of free perks that

annual passholders used to enjoy. Existing annual passholders can renew

their passes, although earlier this month, the company raised the

renewal price for its highest-tier annual passes to Disneyland by 14%,

to $1,599 from $1,399, while at the same time introducing more blackout

days when passholders can’t visit"

"The new

reservation system has allowed the company to limit attendance without

having to turn visitors away when the parks become overcrowded, as it

occasionally did in previous years.

The

company also points out that it offers frequent promotions, including

discounted room rates at its hotels, packages that become more

economical the more days a visitor spends at the park, and discounts for

residents of Southern California and Florida."

"Some longtime fans who come to the park regularly, and aren’t splurging

on once-in-a-lifetime memories, complain about the new fees."

"The

Genie+ app feature replaced a system known as FastPass that used to come

free with any ticket sold at Disneyland or Walt Disney World. The new

service—along with a free version, known simply as Genie—does more than

make Disney money: It also helps the parks’ operators direct traffic and

spread people around the parks more evenly, to reduce waiting times

overall, and upsell visitors by offering them promotions on food,

merchandise and ride-reservation fees.

Each

park has an operation center with a “heat map” that tracks where Genie+

users are in the parks using GPS technology. Park operators can direct

traffic using the app by notifying visitors where the shortest lines are

and offering food and merchandise promotions to cajole them to other

areas.

“If

I’m seeing too much activity on the west side, I’m able to spread where

I direct people to the east side,” Mr. D’Amaro said. “Our attractions

will be load-balanced better, and lines will be shorter, and what that

means is the experience will be better.”

In

an analysis for The Wall Street Journal, Touring Plans analyzed room

prices, including taxes, at three popular Walt Disney World hotels over

the past decade, and found increases that far outpaced inflation, which

in July hit a record high of 9.1%."

"Prices for tickets and certain food items have also climbed faster than

inflation over the past decade, the Touring Plans analysis found. Disney

fan blogs have noted that classic purchases at Disney parks, including

the pineapple Dole Whip frozen treat ($5.99 last year, $6.99 this year

at some locations) and studded Mickey Mouse-ears headbands ($29.99 last

summer, now $39.99) are quickly getting costlier, outpacing inflation."

In economics we say that people want to maximize their utility. They buy the combination of goods that will make them happiest.

These three economists had some interesting observations about this.

Frank Knight was an economics professor at The University of Chicago

in the first half of the 20th century. John Stuart Mill was a British

philosopher and economist in the 19th century.

Here is an interesting quote from Knight followed by a similar one from John Stuart Mill.

"Life

is at bottom an exploration in the field of values, an attempt to

discover values, rather than on the basis of knowledge of them to

produce and enjoy them to the greatest possible extent. We strive to

'know ourselves,' to find our real wants, more than to get what we want"

Source: Knight, Frank H. 1935. "The Limitations of Scientific Method in Economics," in The Ethics of Competition and other Essays. Harper and Row: New York.

I read something about Nobel Prize winning economist James Buchanan today that reminded me of what Knight and Mill said. See Some Economics of James Buchanan by Timothy Taylor (the post is very interesting, raising questions about what economics is). This excerpt is a quote from Buchanan:

"In one sense, the theory of choice presents a paradox. If the utility function of the choosing agent is fully defined in advance, choice becomes purely mechanical. No "decision," as such, is required; there is no weighing of alternatives. On the other hand, if the utility function is not wholly defined, choice becomes real, and decisions become unpredictable mental events. If I know what I want, a computer can make all of my choices for me. If I do not know what I want, no possible computer can derive my utility function since it does not really exist."

All of this raises questions about utility functions. Do we have them? Do they change over time? If they do, how and why?

We say that tastes and preferences are one of the shift factors for demand in economics. If the taste for something increases, then demand increases. But normally we don't say much about why tastes change.

Mill and Knight both seem to be saying that life is finding out what your tastes are. If that is the case, maybe, like Buchanan says, a computer could not make decisions for us.

"The state’s High Plains region, which covers 41

counties in the Texas Panhandle and West Texas, is home to more than

11,000 wind turbines — the most in any area of the state.

The

region could generate enough wind energy to power at least 9 million

homes. Experts say the additional energy could help provide much-needed

stability to the electric grid during high energy-demand summers like

this one, and even lower the power bills of Texans in other parts of the

state.

But a significant portion of the

electricity produced in the High Plains stays there for a simple reason:

It can’t be moved elsewhere. Despite the growing development of wind

energy production in Texas, the state’s transmission network would need

significant infrastructure upgrades to ship out the energy produced in

the region."

"“Because there’s not enough transmission to move it where it’s needed,

ERCOT has to throttle back the [wind] generators,” energy lawyer Michael

Jewell said. “They actually tell the wind generators to stop generating

electricity. It gets to the point where [wind farm operators] literally

have to disengage the generators entirely and stop them from doing

anything.”"

"wind farms across the state account for nearly 21% of the state’s power generation."

"Wind energy is one of the lowest-priced energy sources because it is

sold at fixed prices, turbines do not need fuel to run and the federal

government provides subsidies. Texans who get their energy from wind

farms in the High Plains region usually pay less for electricity than

people in other areas of the state."

"A 2021 ERCOT report shows there have been

increases in stability constraints for wind energy in recent years in

both West and South Texas that have limited the long-distance transfer

of power.

“The transmission constraints are

such that energy can’t make it to the load centers. [High Plains wind

power] might be able to make it to Lubbock, but it may not be able to

make it to Dallas, Fort Worth, Houston or Austin,” Jewell said. “This is

not an insignificant problem — it is costing Texans a lot of money.”"

"the Public Utility Commission, which oversees the grid, is conducting

tests to determine the economic benefits of adding transmission lines

from the High Plains to the more than 52,000 miles of lines that already

connect to the grid across the state. As of now, however, there is no

official proposal to build new lines.

"“It does take a lot of time to figure it out — you’re talking about a

transmission line that’s going to be in service for 40 or 50 years, and

it’s going to cost hundreds of millions of dollars,” Jewell said."

"while transmission upgrades across the state have generally been made

in a timely manner, it’s been challenging to add infrastructure where

there has been rapid growth, like in the High Plains."

This is the title of an article that was published recently and was actually in Spanish by Rafael Galvão de Almeida. He is at Universidade Federal de Minas Gerais, Brasil. The title in Spanish is "Camelot Elétrica: Um Economista Visita a Corte do Rei Arthur."

It was published in the journal "História Econômica & História de Empresas" which means "Economic History & Business History." Click here for more information.

Here is the abstract:

"Mark Twain wrote the book A Connecticut Yankee in King Arthur's Court(1889) as a way of reflecting on the changes taking place in the United States of the so-called “Golden Age”. The book tells the story of Hank Morgan, an engineer who ended up in 6th century England, when King Arthur led the Knights of the Round Table in Camelot. Hank attempts to industrialize England twelve centuries earlier, using his knowledge of technology and culture. However, his Electric Camelot project, over numerous setbacks and failure. The novel is relevant to economists because it deals with various topics of interest, such as entrepreneurship and economic development. The literature on the “visiting economist syndrome” identifies numerous problems in a country’s development aid process due to a number of factors, including even the arrogance and naivety of economic models, but that are present when dealing with different contexts. It is argued that these problems were discussed by Mark Twain, who was interested in the nascent neoclassical economics, in the novel in question. Although Hank is an engineer, his trajectory is similar to that of a visiting economist. Thus, the book is a tool to explore through fiction problems and challenges of economic development."

They are the ‘universal price’ at the base of an economy. Keeping rates artificially low has created an addiction with its own cost.

By historian Adam Rowe. He reviews the book The Price of Time: The Real Story of Interest by Edward Chancellor. Excerpts:

"The practice of charging interest is as old as time itself. Before

Mesopotamians had learned to coin money or place wheels on carts,

lenders had established the practice of demanding more in the future of

whatever they made available to borrowers in the present. The etymology

of many of the words for interest derive from the offspring of

livestock, reflecting an awareness that wealth well managed is fruitful.

But the etymology also reflects a suspicion that interest allows the

rich to devour the poor. Ancient Hebrew words for interest include one

meaning “the bite of a serpent.”"

"From the beginning, Mr. Chancellor shows, rulers have tried to intervene

to soften the antagonism between borrowers and lenders. The earliest

set of laws, Hammurabi’s code in Babylon (from around 1750 B.C.), is

preoccupied with regulating interest—setting maximum loan rates,

including 20% for silver and 33.33% for barley. A millennium later,

Athens’s renowned lawgiver Solon ordered all the stones recording

mortgages destroyed as part of an effort at moral and political renewal.

(His predecessor Draco, to whom we owe the word “draconian,” had forced

many debtors into slavery.) Thinkers and philosophers throughout

history—from Aristotle and Aquinas to Proudhon and Marx—have regarded

any rate of interest as unjust. Mere scribblers shared this view.

According to Daniel Defoe, “interest of money is a canker-worm upon the

tradesman’s profit.”"

"Of proto-capitalist 16th-century England, the historian R.H. Tawney

wrote: “The borrower was often a merchant, who raised a loan in order to

speculate on the exchanges or to corner the wool crop.” As for the

lender, he might well be “an economic innocent, who sought a secure

investment for his savings.”"

"Like any other price, the rate of interest reflects a complex balance of

forces in the real economy, from aggregate savings to future

expectations. When governments push that price too low—or too high—they

create distortions that are counterproductive and socially unjust."

"The price of securities tends to rise or fall inversely with the price

of interest. Those who own the most securities thus benefit the most

when interest rates fall."

"Low interest rates don’t help the poor, who don’t have access to cheap

credit. They do help people with formidable assets already, in part by

making leverage more attractive. With money so cheap, financiers can

boost investment returns with borrowed cash."

"Artificially low rates distort the decentralized decision-making process

of a market economy. Without interest, he writes, “capital can’t be

properly allocated and too little is saved.” Investors accept more risk

in pursuit of higher returns, making future growth seem more attractive

than current profits. And because interest is one of the chief costs in

finance, low rates shift economic activity from “real world” enterprises

to purely financial transactions."

"How does working from home change this picture? When workers can work

from home instead of driving into the office, this makes available a

new substitute for driving. Working from home is relatively cheaper than

driving, so many workers would prefer to work from home, if they can.

That makes demand for petrol more elastic. The change in elasticity will

be greatest for workers where working from home is a closer substitute

to working in the office. That will include workers who don't have to

drive towards work for other reasons, such as dropping kids off at

school, grocery shopping on the way home, etc.

The current high

price of petrol (as a result of the war in Ukraine, and unrelated to

working from home (as far as we know)), has probably reinforced the

increase in the price elasticity of demand. If petrol is now taking up a

higher proportion of household income, demand will tend to be more

elastic for that reason as well.

Combining those effects, demand

for petrol is more elastic now than it was before the pandemic led to a

large increase in working from home."

"Broad new

data on wages earned by college graduates who received federal student

aid showed a pay gap emerging between men and women soon after they

joined the workforce, even among those receiving the same degree from

the same school.

The

data, which cover about 1.7 million graduates, showed that median pay

for men exceeded that for women three years after graduation in nearly

75% of roughly 11,300 undergraduate and graduate degree programs at some

2,000 universities. In almost half of the programs, male graduates’

median earnings topped women’s by 10% or more, a Wall Street Journal

analysis of data from 2015 and 2016 graduates showed."

"Determining

why those gaps appear earlier isn’t simple. The federal data don’t

account for such factors as recipients of the same degrees seeking

different types of jobs and career paths, some of which pay far more

than others. Studies have shown that men tend to negotiate salaries more

aggressively than women, and women at times shy away from ambitious goals for fear of being unprepared. Even when women and men have identical academic credentials, women sometimes choose lower-paying career paths, pursuing a passion rather than a high paycheck.

The

median pay for men from the California State University, Fullerton,

nursing master’s program, for instance, was $199,000 three years after

graduation, compared with $115,000 for women. The school said that is

largely because women in the program gravitated toward nurse midwifery,

which pays less than specialties like anesthesiology.

Researchers also say that discrimination, despite laws against it, remains a factor in the gender pay gap at all career levels."

"Among those with undergraduate degrees, women out-earned men in just four of the 20 most popular areas of study"

"Across those 20 fields, men and women’s pay came closest to parity in economics, where women earned 1.4% more than men.

“There is no neat, tidy explanation” for the early-pay disparities, said Francine Blau, a Cornell University labor economist.

Researchers

say women choosing careers sometimes internalize societal expectations

about which jobs suit them. Well-intentioned advisers and employers can steer women toward less lucrative options, based on assumptions about their aspirations.

Graduates

of petroleum-engineering programs, among the highest-paying

undergraduate majors in the country, often take jobs either as field

engineers or data analysts. Career-service advisers and graduates said

women are more represented in the latter roles, which are based in an

office, involve more regular work hours and can pay less."

"Different

job tracks also can explain part of the pay gap at Michigan’s law

school, where men earned a median income that was 37% higher than

women’s three years out.

The

school said that in the classes of 2015 and 2016, 237 men took jobs at

law firms, while 158 women did. Fourteen men headed into public-interest

jobs, whereas three times as many women did. The classes those years

had slightly more men than women.

Several

women said in interviews that the mission-driven work appealed to them,

outweighing the draw of a higher law-firm salary."

"Several women who graduated from the San Antonio program noted that male

classmates launched their own practices—generally a more lucrative

path—sooner after graduation than female classmates, who often completed

residencies and worked for other dentists before buying or starting a

practice."

"The Federal Reserve sets two overnight interest rates: the

interest rate paid on banks' reserve balances and the rate on our

reverse repurchase agreements. We use these two administered rates to

keep a market-

determined rate, the federal funds rate, within a target range set by

the FOMC."

"The Federal Reserve (the Fed)

is the central bank of the United States. As the central bank, it serves

several key functions within the economy. One of the most important

functions of the Fed is to promote economic stability using monetary

policy. The Fed's goals for monetary policy, as defined by Congress, are

to promote maximum employment and price stability.

The Federal Open Market Committee (FOMC) is the monetary

policymaking arm of the Federal Reserve. The FOMC usually meets eight

times per year in Washington, D.C. These two-day meetings include a

review of economic data and financial conditions, briefings by

economists, policy discussions, and a vote on the setting of monetary

policy—including a decision about whether the FOMC will adjust its

target range for the federal funds rate. The federal funds rate is the

interest rate banks charge each other for overnight loans. The Fed sets a

target range for where it wants the interest rates charged to fall

within, and it is the setting of this range that the Fed uses to

communicate its monetary policy position.

Figure 1 The Federal Funds Rate Target Range

SOURCE: Board of Governors of the Federal Reserve System via FRED®, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/graph/?g=COX8, accessed April 4, 2022.

The FOMC conducts monetary policy by

setting the target range for the federal funds rate. This graph shows

the target range, determined by the upper and lower limits, and the

effective federal funds rate within the range.

Over time, as shown in Figure 1,2 the FOMC has moved the

target range up and down as it steers the economy toward maximum

employment and price stability. For example, once the economy recovered

from the global financial crisis, the FOMC moved the target range from

near zero at the end of 2015 up to 2¼ -2½ percent by early 2019. Then

when the COVID-19 pandemic hit, the FOMC quickly moved the target range

back to near zero.

What Is the Federal Funds Rate and Why Is It So Important?

The federal funds rate is a very specific short-term interest rate.

It involves the transfer of funds between banks that maintain accounts

(deposits) with their Federal Reserve Bank; the accounts are called reserve balance

accounts. The federal funds market is where banks that may need money

in their reserve accounts for cashflow reasons go to borrow from banks

that have excess funds in their reserve accounts. Banks who lend funds

act as suppliers of reserves in the federal funds market; banks who

borrow funds act as demanders of reserves in the federal funds market.

The federal funds rate is not "set" by the Fed, but rather determined by

the borrowers and lenders in the federal funds market.

Monetary policy is transmitted through market

interest rates to affect consumers' and producers' spending decisions,

which ultimately moves the economy toward the Fed's objectives—maximum

employment and stable prices. This monetary policy implementation

framework ensures that when the FOMC changes its policy stance (raises

or lowers the target range for the federal funds rate), market interest

rates and financial conditions move in the desired direction.

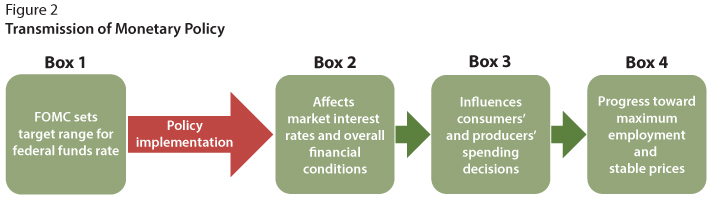

The FOMC conducts monetary policy by setting the target range for the

federal funds rate (Figure 2, Box 1). Then the Fed implements policy by

using its monetary policy tools to ensure the federal funds rate stays

within the target range (red arrow).

The federal funds rate is important because when the FOMC sets its

target range, it influences many other interest rates in the economy

(Figure 2, Box 2). In fact, by adjusting the target for this rate, the

Fed can influence the spending choices of consumers and producers

(Figure 2, Box 3) and ultimately move the economy toward maximum

employment and price stability (Figure 2, Box 4).

The Fed's Monetary Policy Implementation Toolbox

The Fed uses its monetary policy tools in the implementation phase.

In all, the Fed uses four key tools to help ensure the federal funds

rate stays within the target range set by the FOMC.3 We'll

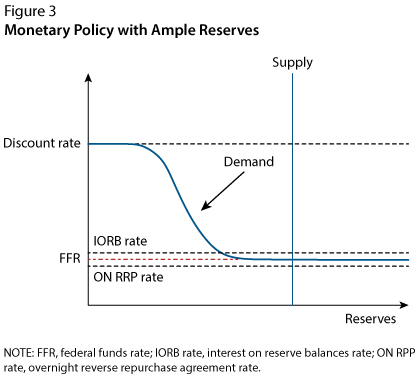

use a simple supply and demand model (Figure 3) to describe how the

tools work together. Overall, these are the critical tools the Fed uses

because reserves in the banking system are ample. That is, the supply of

reserves, set by the Fed, is large enough that it intersects the demand

curve where it is nearly flat (see Figure 3).

In the ample-reserves framework, the Federal Reserve raises (lowers) its administered rates to move the federal funds rate higher (lower). Small shifts of the supply curve have little or no effect on the federal funds rate.

The Fed's Primary Tool: Interest on Reserve Balances

Today, the Fed's primary tool for adjusting the federal funds rate is

interest on reserve balances. The interest on reserve balances rate

(labeled "IORB rate" in Figure 3) is the interest rate paid on funds

that banks hold in their reserve balance account at a Federal Reserve

Bank. For banks, this interest rate represents a risk-free investment

option. Importantly, the interest on reserve balances rate is an

"administered rate," which means it is set by the Fed and not determined

in a market (like the federal funds rate is). In fact, there are two

key concepts that ensure interest on reserves is an effective tool.

The first concept is the reservation rate, which is the lowest

rate that banks are willing to accept for lending out their funds.

Banks can deposit their funds at the Federal Reserve and earn the

interest on reserve balances rate. Because depositing funds at the Fed

is a risk-free option, banks will likely not be willing to lend their

funds in the federal funds market for a lower interest rate than they

can earn from depositing their funds at the Fed. So, the interest on

reserve balances rate serves as a reservation rate for banks.

The second concept is arbitrage, which is the simultaneous

purchase and sale of funds (or goods) in order to profit from a

difference in price. For example, let's assume reserves are trading in

the federal funds market at 2 percent (i.e., the federal funds rate is 2

percent) and that reserves (deposits) at the Fed earn 2.5 percent

(i.e., the interest on reserve balances rate is 2.5 percent). Banks will

quickly see that they can borrow funds in the federal funds market at 2

percent and deposit those funds at the Fed and earn the interest on

reserve balances rate of 2.5 percent, which means that they can earn a

profit of 0.5 percent (the difference between the rates).The increase in

demand for funds in the federal funds market will put upward pressure

on the federal funds rate, and the federal funds rate will rise toward

the interest on reserve balances rate. This upward pressure on the

federal funds rate will continue until the federal funds rate has risen

to the level that banks no longer see the opportunity to profit.

So, arbitrage ensures that the federal funds rate does not fall far below the interest on reserve balances rate.

Arbitrage is the reason why these short-term rates remain closely

linked. In fact, arbitrage is what makes interest on reserve balances an

effective tool for guiding the federal funds rate. Because the Fed sets

the interest on reserve balances rate directly, the Fed can steer the

federal funds rate down or up by lowering or raising the level of the

interest on reserve balances rate. As a result, interest on reserve

balances is the Fed's primary tool for adjusting the federal funds rate,

but the Fed has other tools that play supporting roles.

Setting a Floor for the Federal Funds Rate: The Overnight Reverse Repurchase Agreement Facility

Interest on reserve balances is available only to banks and a few

other institutions. The Fed has an overnight reverse repurchase facility

that is open to a broader set of financial institutions. This facility

allows these financial institutions to deposit their funds at a Federal

Reserve Bank and earn the overnight reverse repurchase agreement rate

offered by the Fed. The overnight reverse repurchase agreement rate

(labeled "ON RRP rate" on Figure 3) works for these institutions similar

to the way the interest on reserve balances rate works for banks. So,

this rate acts like a reservation rate for these financial institutions,

and the overnight reverse repurchase agreement rate interacts with

other short-term market rates through arbitrage. The overnight reverse

repurchase agreement facility is a supplementary tool because the rate

the Fed sets for it helps set a floor for the federal funds rate (Figure

4).

Figure 4 Steering the Federal Funds Rate

SOURCE: Federal Reserve Bank of New York and Board of

Governors of the Federal Reserve System via FRED®, Federal Reserve Bank

of St. Louis;

https://fred.stlouisfed.org/graph/?g=LP47, accessed April 4, 2022.

The Fed implements monetary policy by using

its monetary policy tools, such as the interest of reserve balances

rate (red) and overnight reverse repurchase agreement rate (blue), to

ensure interest rates are consistent with the federal funds rate

target.

Setting a Ceiling for the Federal Funds Rate: The Discount Window

The discount rate is the rate charged by the Fed for loans obtained through the Fed's discount window.

Because banks will not likely borrow at a higher rate than they can

borrow from the Fed, the discount rate acts as a ceiling for the federal

funds rate: It is set higher than the interest on reserve balances rate

and the overnight reverse repurchase agreement rate (Figure 5).

When the Federal Reserve lowers its administered

rates, the end points of the demand curve shift down. The vertical

supply curve is unchanged. The demand curve intersects the supply curve

at a lower federal funds rate. In general, the Fed tends to lower all

the administered rates by the same amount, keeping the spread between

the rates constant.

The Final Tool: Open Market Operations

As noted above, the Fed's current method for implementing monetary

policy relies on banks' reserves remaining "ample." So, if the Fed needs

to add reserves to ensure they remain ample, it does so by buying U.S.

government securities in the open market. This action is known as open market operations.

When the Fed buys securities, it pays for them by depositing funds into

the appropriate banks' reserve balance accounts, adding to the overall

level of reserves in the banking system. As Figure 3 shows, open market

operations can be used to shift the supply curve left or right. Prior to

2008, open market operations were the Fed's primary monetary policy

tool, which it used daily to make sure the federal funds rate hit the

FOMC's target. Today this tool is mainly used to ensure that reserves

remain ample.

Now that you understand the Fed's implementation tools, let's see how

the Fed uses them to achieve its two goals: maximum employment and

price stability.

Expansionary Monetary Policy Using the Fed's Tools

Suppose the following: The economy weakens, with employment falling

short of maximum employment, and the inflation rate has been steady at

around 2 percent but is showing signs of decreasing. The FOMC might

decide to conduct monetary policy by lowering its target range for the federal funds rate. To implement

that monetary policy, it would decrease its administered rates—the

interest on reserve balances rate, overnight reverse repurchase

agreement rate, and discount rate—to ensure the market-determined

federal funds rate stays within the target range (see Figure 5). These

actions would transmit to other interest rates and broader financial

conditions:

Lower interest rates decrease the cost of borrowing money, which

encourages consumers to increase spending on goods and services and

businesses to invest in new equipment.

The increase in

consumption spending increases the overall demand for goods and services

in the economy, which creates an incentive for businesses to increase

production, hire more workers, and spend more on other resources.

As

these increases in spending ripple through the economy, likely moving

the unemployment rate down toward its full employment level, inflation

could possibly move up.

So, the Fed's monetary policy implementation tools can be effective

for moving the economy back toward maximum employment and price

stability when the economy is stalling.

Contractionary Monetary Policy Using the Fed's Tools

Suppose the following: The economy is showing signs of overheating,

with the unemployment rate very low and businesses finding it hard to

fill jobs, and the inflation rate has been above the Fed's 2 percent

target for quite some time and is rising. In this case, the FOMC might

decide to conduct monetary policy by raising its target range for the federal funds rate. To implement

that monetary policy, it would increase its administered rates—the

interest on reserve balances rate, overnight reverse repurchase

agreement rate, and discount rate—to ensure the federal funds rate stays

within the target range. These actions would transmit to other interest

rates and broader financial conditions:

Higher interest rates increase the cost of borrowing money and

raise the incentive to save, which dampens consumer spending on some

goods and services and slows businesses' investment in new equipment.

The

decrease in consumption spending decreases the overall demand for goods

and services in the economy, which will likely lead to a decrease in

production levels, fewer employees hired, and less spending on other

resources.

As these decreases in spending ripple through the

economy, demand for workers could lessen, inflationary pressures would

diminish, and the inflation rate would fall back toward 2 percent.

So, higher interest rates can be used to move the economy back to

maximum employment and price stability when the economy is overheating.

Conclusion

The Fed has a congressional mandate of maximum employment and price

stability. The FOMC conducts monetary policy by setting the target range

for the federal funds rate. Then the Fed uses its monetary policy tools

to implement the policy, which guides market interest rates toward the

Fed's desired setting of policy. The Fed ensures there are ample

reserves in the banking system and uses its administered rates to steer

the federal funds rate into the FOMC's target range: Interest on reserve

balances is the Fed's primary tool for adjusting the federal funds

rate; the overnight reverse repurchase agreement facility is a

supplementary tool that sets a floor for the federal funds rate; and the

discount rate serves as a ceiling for the federal funds rate. Changes

in the federal funds rate are transmitted to other interest rates

through arbitrage and affect the decisions of consumers and businesses.

Their decisions ultimately move the economy toward maximum employment

and price stability.

2 The effective federal funds rate is the

rate used in the figures in this article. On any given day, there are

many transactions that settle at slightly different federal funds rates.

The effective federal funds rate is the volume-weighted median rate of

these transactions.

3 The Fed recently introduced two

repurchase agreement (repo) backstop tools, the standing overnight repo

facility and the foreign and international monetary authorities repo

facility. These are used by specific counterparties to help set a

ceiling on repo rates. We do not discuss them here because this article

is targeted toward a principles of economics audience.

Arbitrage: The simultaneous purchase and sale of funds (or goods) in order to profit from a difference in price.

Discount rate: The interest rate charged by the Federal Reserve to banks for loans obtained through the Fed's discount window.

Facility: A standing program targeted at a set of

counterparties for depositing or lending. The Fed has permanent

facilities (like the discount window and the overnight reverse

repurchase agreement facility) as well as temporary facilities (like

those implemented during the Financial Crisis of 2007-09 and the

COVID-19 pandemic).

Federal Open Market Committee (FOMC): A Committee created by

law that consists of the seven members of the Board of Governors; the

president of the Federal Reserve Bank of New York; and, on a rotating

basis, the presidents of four other Reserve Banks. Nonvoting Reserve

Bank presidents also participate in Committee deliberations and

discussion.

Maximum employment: The highest level of employment that an economy can sustain while maintaining a stable inflation rate.

Open market operations: The buying and selling of government

securities through primary dealers by the Federal Reserve. When the

securities are bought or sold, reserves in the banking system are

increased or decreased, respectively.

Price stability: A low and stable rate of inflation maintained over an extended period of time.

Reservation rate: The lowest rate of return that banks are willing to accept for lending out funds.

Reserve balances (reserves): The deposits a bank maintains in its account with a Federal Reserve Bank."